Ignite DTC Growth: Use debt to grow without lighting yourself on fire

A practical guide for the entrepreneur with $5m - $30m in revenue on how to use debt the right way & avoid common pitfalls.

Debt is like gasoline. Used right, it’s a powerful tool that can act as an accelerant for a fast growing business. Improper usage and you’ll burn your business down.

DTC/eCommerce requires strong cash flow planning - which means correct utilization of debt is difficult.

This article will provide entrepreneurs running consumer brands with $5m - $30m in revenue with an idea of how to make the perfect credit cocktail…

A cocktail that minimizes cost and risk while maximizing benefits of non-dilutive capital to grow faster; not a Molotov for self-immolation.

By minimizing risk, I mean the difference between 3 months of runway if things go wrong with your creditors versus 15 months to get things on the right track.

Here’s what you’ll get out of this article…

How to analyze and understand the true cost of debt - not just the interest rate!

What happens when things do not go well?

The differences between different types of lenders, and who gets paid in what order; absolute priority.

Cut risk - maximize the effectiveness of your debt stack - and reduce what you pay for it - the art of building the perfect debt stack.

Personal guarantees.

“Mehtab, my business is super profitable, I don’t need debt!”

If your business is profitable, growing quickly and there doesn’t appear to be a good reason to utilize debt…you might be surprised!

Outside of normal working capital needs, here are some other ways to use credit…

Dividend recapitalization - similar to refinancing your house, you can pull cash out of a business to diversify your income.

Do you need a $75m exit or is it better to take $10m out of the business without having to sell any equity? Remember, interest payments are tax deductible too. Note, the market for dividend recapitalizations is very sensitive to macroeconomic cycles. There are also other ways to perform recapitalizations without going through a formal process that involve playing with your working capital requirements for the business.

Operating discipline - a better run company.

There’s an argument to be made that running with a certain amount of debt creates operating discipline, even for companies where founders are still in control. A formal secured lender may want specific reporting or require/reward meeting certain financial metrics. This third-party oversight can prevent management from becoming complacent. There are plenty of dry academic articles covering this concept floating around online, most won’t have anything operationally useful to learn from, except what I mentioned above.

A lower interest rate doesn’t mean cheaper debt - decoding the true cost of debt - hidden pricing factors.

Lower fees and interest rates do not mean that credit from one lender will be cheaper than the other.

Hidden pricing factors:

What is the cost of complying with reporting requirements? If you’re a small business with $15m in revenue, paying for audited financial statements is a tangible expense that you need to factor in.

How will complying with covenants (in debt financing, a covenant is a rule in the loan agreement that the borrower must follow) impact your ability to operate the business? If a lender wants you to hit a certain profitability metric each month, is that going to materially impact your ability to reinvest in the business? For example, you might want to switch ERP systems. You expect this to negatively impact cash flow for a 6 month period, can you still do this and be compliant with your lender?

If you breach a covenant, typically the lender will effectively charge you a fee. Some lenders design their offer such that you breach covenants so they can rack up additional fees. Make sure you model out the full impact of compliance on your working capital needs, profitability, and growth goals. Creating a 13-week cash flow model can help you see if you’re at risk of breaching a covenant. Common covenants include debt to service coverage, maximum debt to EBITDA, minimum working capital, limitations on unfunded capital expenditures, and limitations on payments to shareholders.

How many hours will your C-level or finance team spend reporting to your lender and managing the relationship? This is a real expense that needs to be factored in. Requests can be very time consuming depending on the lender and how familiar they are with your industry. The less familiarity there is from the lender with your business, the more infuriating and frustrating they will be to fulfill for you and your management team.

Lenders will often want additional compensation in the form of an original issuer discount (you’ll see this abbreviated to OID), warrants, diligence and legal fees. These add up quickly.

Psst, this is all free - all I want is you to subscribe! My promise is that anything I send you will be longform - just like this article - and packed full of tips you can quickly implement at your business. No esoteric “strategy” BS. I have nothing to sell you. Click the big pink button….

Thing are not going to plan - now what?

Understanding exactly what happens if you are in technical default or if your lender is running into trouble themselves is important.

A well structured credit stack with good terms, planning on your end, and understanding exactly what you are signing up for can create ~4x - 6x the runway if things go wrong.

Here’s a high-level overview of how defaults play out…

You miss a payment or breach a covenant.

The lender will want additional compensation and a plan to get you back on track. This plan will vary depending on the lender. If you’re borrowing from a traditional lender, they’ll want to see blood. The best form of which is your salary reduced, executive pay reduced, layoffs, and clear focus on cutting expenses. My blog article here has more details around negotiating with lenders when you are in default.

If you built your credit stack right, and negotiated terms well, you’ll have enough headroom to ensure you don’t blow up your company.

If you did not build your stack right, you now have to try and fix the company without much runway and hope creditors give you what you need to make it happen.

If things do not go well, there are plenty of legal tools available to build runway. You should have read up on these prior. For example, some businesses may be eligible for subchapter V, which is an expedited restructuring that allows owners to maintain their full equity position without injecting additional capital. There are also lenders and private equity firms that you can go to that specialize in working with distressed businesses; our firm, Karta Ventures, specializes in distressed direct-to-consumer with ~$12m - $75m in revenue.

Considerations for when your company underperforms.

Is the lender litigative? There’s an easy way to check! Look them up via PACER and see what they have done in the past. Did they drag borrowers to court quickly? Were they reasonable in bankruptcy or did they slow the process down arbitrarily? We recently saw a lender spend a strangely large amount relative to their outstanding balance in a bankruptcy case. It made no business sense. That is a lender you would want to avoid.

Tripping a covenant may result in technical default. This means you didn’t miss a payment but are still considered in default. What happens now? What fees will you incur?

You miss a payment all together. Things aren’t going well. What now? How open is your lender to working on a plan together?

Does your lender understand the business you are in? This can make a huge difference when things go sideways. They will understand the difference between impaired performance because of incompetence and impaired performance because of factors outside of your control.

You discover a great project that will dramatically improve net cash flow after it’s complete. The project requires you to reduce profitability for 6 months. How will your lender work with you in-case this trips a covenant?

Your lender is on fire. Did you know that could happen? You do now!

Your lender emails you and tells you that your credit line isn’t going to be renewed, this makes no sense because EBITDA is up 1.5x and revenue looks great too.

The lender informs you it’s because their business isn’t doing well, or more likely, they’ll try to blame it on external factors.

Then it hits you, your lender is also running a business, except they might not be great at it.

During the process, be sure to run basic diligence on your lender. In my experience, it’s worth paying more for a rock solid lender with an excellent reputation that has survived multiple cycles.

The biggest question for you is how they are funded and what risks you face as a result.

The best example of this are the crop of programmatic eCommerce lenders that popped up from 2019 through 2021. A great example is ClearBanc/Clearco.

These venture-backed lenders specific to eCommerce offered large credit lines with little to no diligence, and were almost always unsecured.

How was this possible? It wasn’t.

As they lost their ability to raise dumb equity, they found themselves out of compliance with their own lenders.

What did this mean for companies borrowing from them?

Credit lines were suddenly pulled without any prior notice, or not renewed at all on the normal cadence. If you borrowed from one of these lenders that happened to be secured, then it meant they could pull the rug from under you, and you’d be in a precarious spot. This put a lot of companies in precarious positions, especially if they did not understand what legal tools were available to them to lessen the impact of losing credit with little notice.

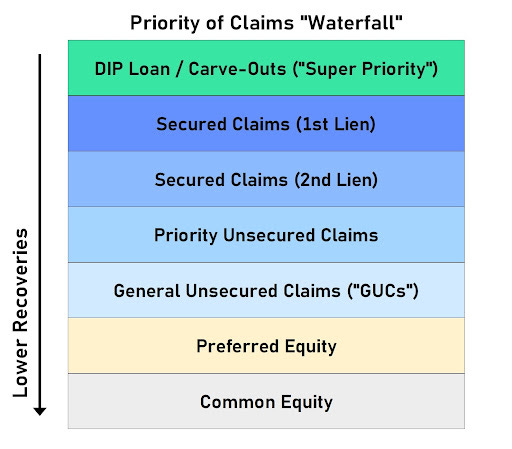

The pecking order of creditors - absolute priority

Before we jump into building your debt stack, it’s important to understand a handful of basic concepts. Note - I kept this simple, there is a lot more to this that I left out! For example, perfected vs unperfected security interest.

A quick and simple rundown of seniority & priority. Visually first:

Source: O’Bryan Law Offices

https://obryanlawoffices.com/wp-content/uploads/2022/01/apr.jpeg

Seniority refers to the priority of repayment. It is a concept that determines the order in which creditors are repaid and the level of risk associated with different types of debt. It’s the pecking order of creditors, giving some lenders priority over others in recovering funds if something goes wrong.

When a borrower defaults, the assets and cash flows of the borrower's business or the collateral provided for the loan are used to repay creditors. The seniority structure defines which creditors are to be repaid first.

Senior debt holders hold a higher position in the seniority structure and have a greater likelihood of recovering funds compared to subordinated or junior debt holders. In bankruptcy or liquidation, senior creditors are given priority in the distribution of proceeds, ensuring that they are repaid before junior creditors. Senior debt may include mortgages, secured loans, and other forms of debt that have a first lien on the borrower's assets.

On the other hand, junior, subordinated and unsecured creditors have a lower position in the seniority structure and are considered riskier. They are repaid after senior debt holders have been fully satisfied. Examples include mezzanine debt, unsecured loans, and other forms of debt like vendor credit, that have a lower priority claim on the borrower's assets.

Lenders providing senior debt offer lower interest rates due to their higher priority in repayment whereas lenders providing junior debt require higher returns to compensate for increased risk.

Note, the above is how things are supposed to play out, but practically, they do not play out that way, especially when dollars at risk are too low for extensive litigation, which is usually the case for companies with less than ~$30m - $40m in revenue.

This means there’s a lot of room to get creative and build a viable path back to growth for a company facing bankruptcy or insolvency! It does require the right people including an excellent legal team, turnaround practitioner (hello!), and potentially investment bankers if your company is larger than ~$40m - $60m in revenue.

One example of creativity is using a new tool like subchapter V, which is a new form of expedited restructuring that allows a filer to keep all of their equity without being required to inject additional capital.

Another great example is DIP financing - which stands for debtor-in-possession. It provides funds to a company that has filed for bankruptcy protection and allows it to continue operating while restructuring its debts. DIP financing is intended to help the company maintain its operations, preserve value, and facilitate the restructuring process.

DIP financing is unique because it gives the DIP lender a senior position in the repayment hierarchy, even if they are extending new credit to the distressed company. This means that in the event of liquidation or repayment, the DIP lender has a higher priority claim on the company's assets compared to other creditors. This seniority helps mitigate the lender's risk and encourages them to provide financing to a distressed company on the brink of implosion.

The above can put the original secured senior lender in a bad spot, as they are now next in line after the DIP lender, and their underwriting may not have accounted for that. Courts attempt to ensure DIP terms are fair, taking into account the best interests of the company and its creditors...but what is fair? With smaller dollar amounts, it’s unlikely that a senior creditor will argue over a DIP much.

Specialty lenders and private equity firms that offer DIP financing exist, however, none that specialize in eCommerce and DTC except for us - Karta Ventures. We welcome complex opportunities that others are unable or unwilling to tackle.

Time to ask you to subscribe again…just click the pink button…it’s free!

If you need help with something related to digital media or more pureplay digital without physical products, I would recommend reaching out to my friend Ari at HRX, he helped me edit this article, and asked for a shoutout…so here I am.

As an entrepreneur, you need to consider the implications of seniority when structuring their financing arrangements and assessing their ability to meet their debt obligations in various scenarios. This is what we will dive into below…

Control risk & maximize reward - the art of building the perfect credit stack

Think of the perfect debt stack as a cocktail. A cocktail with the right mix of credit allows you to hit growth goals while reducing risk and cost.

Often, brands will work with a single lender that provides what appears to be the lowest effective interest rate.

This isn’t a great approach for reasons discussed above, for example, a single secured lender can pull the rug under your feet and force you to dance.

Start by building a 13-week cash flow model. Preferably with a longer time horizon, let’s call it ~6 quarters. It’s important to understand what this period looks like so you can account for seasonal fluctuations in cash flow, inventory ramp up periods, and fueling growth.

Now, model different scenarios, and look at what that does to cash needs.

When building your stack, aligning debt maturities with cash flow projections is vital for controlling risk.

Short-term unsecured credit provides a shot in the arm for cash flow fluctuations. Long-term secured debt can be used for larger investments or strategic initiatives with clear rewards.

Balancing debt maturities allows you to manage repayments effectively and adjust your capital structure as needed - plus makes it less likely that you run into a cash crunch if a lender decides not to work with you again - or implodes.

Our preference is being able to pay secured creditors even in the event that things do not go well. If your company is larger, you can split out lenders in the secured bucket and diversify your funding sources. It will also buy you more time in the event things go wrong.

Unsecured creditors are a great use-case to fund initiatives that are not guaranteed wins. There are tons, and tons of sources of unsecured credit available to most businesses. Examples include vendor debt, corporate credit cards, and the newer crop of programmatic lenders.

Vendor debt in particular is preferable because it can be defaulted on with very little impact to the company, especially if the vendor is not critical to operations. During COVID, large companies immediately pushed vendor payments back in order to create a cash buffer for themselves. In a distressed situation, you can often defer payment to a critical vendor and offer them something in return, like additional volume or paying more for inventory in the future.

The best advantage to having multiple lenders in a stack is that it makes litigation less likely. Lenders know that getting aggressive in a default scenario is more likely to backfire when their actions can be the trigger for other existing lenders to drain liquidity from the company and create a huge mess where nobody is likely to come out well. This makes everyone much more cooperative and reasonable.

A quick note on personal guarantees

Many forms of credit for small businesses with less than ~$2m in EBITDA or ~$10m in topline revenue will require a personal guarantee. Those lending to businesses with $10m - $25m may offer some form of pricing discount in exchange for a personal guarantee, but the price savings will greatly diminish as you move up in revenue.

Quick rules of thumb:

Under $10m in revenue - expect to PG.

Over $10m in revenue - ask for a discount if you do PG.

As revenue scales over $10m, the discount for offering a personal guarantee will get much smaller, because the company is much safer for the lender to invest in.

There are many ways to protect yourself from personally guaranteed debt hurting you if things go sideways, but they vary tremendously state-by-state. For example, your primary residence is protected up to a specific amount in the event of personal bankruptcy. Your best bet is to speak with an excellent attorney about structuring things correctly before signing anything with a PG.

We are done! Now what?

If you’re running a DTC brand with $12m+ in revenue, healthy or distressed, our firm - Karta Ventures - would appreciate the opportunity to invest in you.

We welcome complex opportunities that others are unable or unwilling to tackle and take pride in our response times. Simply use the contact us form on our site here: www.kartaventures.com.

Examples of situations where we are a great fit…

You have shareholders that are no longer value-add for where you are in your entrepreneurial journey. They were great when you had $5m in revenue, but are not helping you move the needle at $20m in revenue. You want to provide them with liquidity and want a value-add partner to work with (that’s us).

Distressed brands in need of financing and expertise to help turn things around.

Fast-growing or profitable DTC brands that want a partner that is willing to jump in and help in a tactical way. We do not sit around & talk about strategy.

Creditors with a portfolio company that is in default. We have worked with several lenders to build a solution that works for everybody.

Remember…just like any other tool we use in DTC, whether it’s meta ads or attribution software, debt is not inherently good or bad; it is how it is managed and utilized.

Taking the time to understand credit gives you a powerful source of non-dilutive capital to fuel your company's rapid growth without the risk commonly associated with debt.

If you’d like to take things further, working with experienced restructuring attorneys and turnaround practitioners is a good idea. They can help you draft a plan for when things go wrong with creative structures that provide you with much more runway.

I appreciate any comments or suggestions in the comment section below!

Another value-packed writeup. Love the content you're putting out here!

Wow! Thanks for sharing!! Just hope this doesn't go behind a paywall please!!!!